Long Put Option Strategy

A long put option strategy entails purchasing a put option by itself. Investors with an investment objective of capital preservation and a bearish market view will utilise the long put option strategy. The investor aims to take a position and profit from the fall in the price of an underlying asset.

The maximum upside potential in a long put is the strike price minus the premium. The maximum potential loss is 100% of the amount invested in the long put option. Therefore, a long put option strategy requires a considerable level of risk tolerance.

Let’s See an Example:

An investor anticipates that the stock price of XYZ will decline in the next 3 months. XYZ trades at USD10, while a 3-month put option with the USD10 strike price trades at USD2.

The investor buys one XYZ call option at the USD10 strike price with 3 months until the expiration date for a premium of USD2.

The maximum potential profit is the strike price of USD10 less the USD2 premium received multiplied by 100 shares. This is calculated as follows:

- Maximum Profit per Option = (Put Option Strike Price - Premium) x 100 shares

- USD800 = (USD10- USD2) x 100 shares

The maximum potential loss is the premium of USD2 paid for the put option multiplied by 100 shares. This is calculated as follows:

- Maximum Loss per Option = Premium Paid x 100 shares

- USD200 = USD2 x 100 shares

The break-even point is the USD10 strike price of the option less the USD2 premium. This is calculated as follows:

- Break-Even Point = Strike Price – Premium Paid

- USD8 = USD10 - USD2

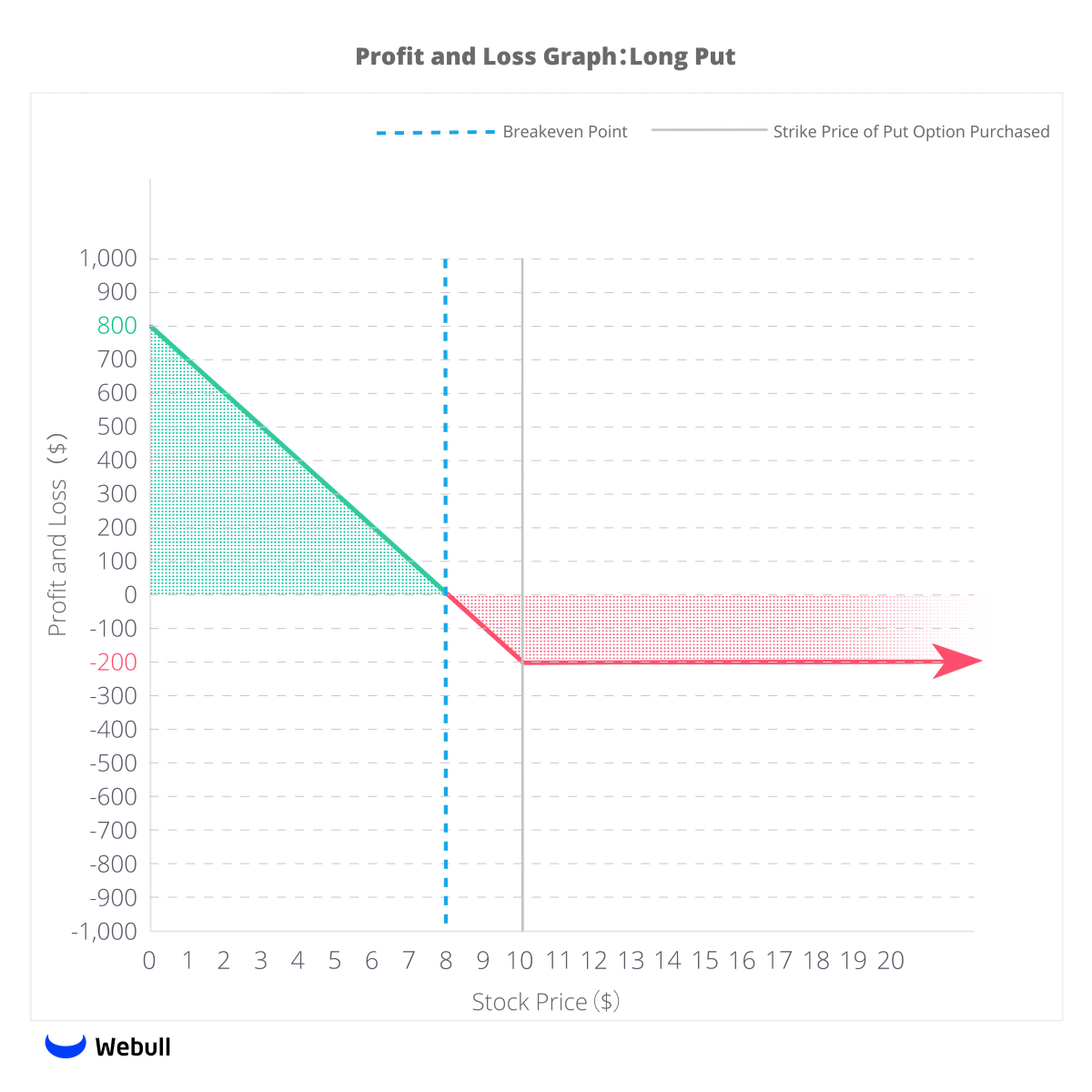

The profit and loss of the long put option strategy until the expiration date is depicted in the chart below.

The chart shows the potential profit and loss on the y-axis versus the corresponding stock price on the x-axis until the expiration date.

If XYZ trades remain above USD8 and beyond, the investor will take a loss between USD0 and USD200. If XYZ trades fall below USD8, the put option strategy becomes profitable with a maximum potential gain of USD800 if the price goes to zero. The break-even point is USD8, which is the strike price of USD10 less the premium paid of USD2.

If XYZ falls below anywhere between USD10 and USD0 during the duration of the option contract, the long put holder can exercise the option. This means the investor would sell 100 shares of XYZ at USD10. If the investor currently holds shares of XYZ, the shares would be sold at USD10. If the investor does not hold XYZ shares, the options will be liquidated if it is in the money. On the other hand, if the options contract is out of the money, the contract will expire worthless. If the investor wishes to capitalise on the decrease in XYZ’s share price without exercising the option, he can sell the option at a profit once the price falls below USD8 a share.

If XYZ remains above USD10, the option will expire worthless, and the investor permanently loses the USD200 invested.

Disclaimer: Options trading involves significant risk and is not suitable for all investors as investors may be exposed to potentially rapid and substantial losses. Options trading functionality is subject to Webull Securities' review and approval. Please read Characteristics and Risks of Standardized Options before investing in options.